Key Takeaways

- The One Big Beautiful Bill Act (OBBBA) made the favorable Tax Cuts and Jobs Act (TCJA) provisions permanent, stabilizing tax policy for businesses and individuals.

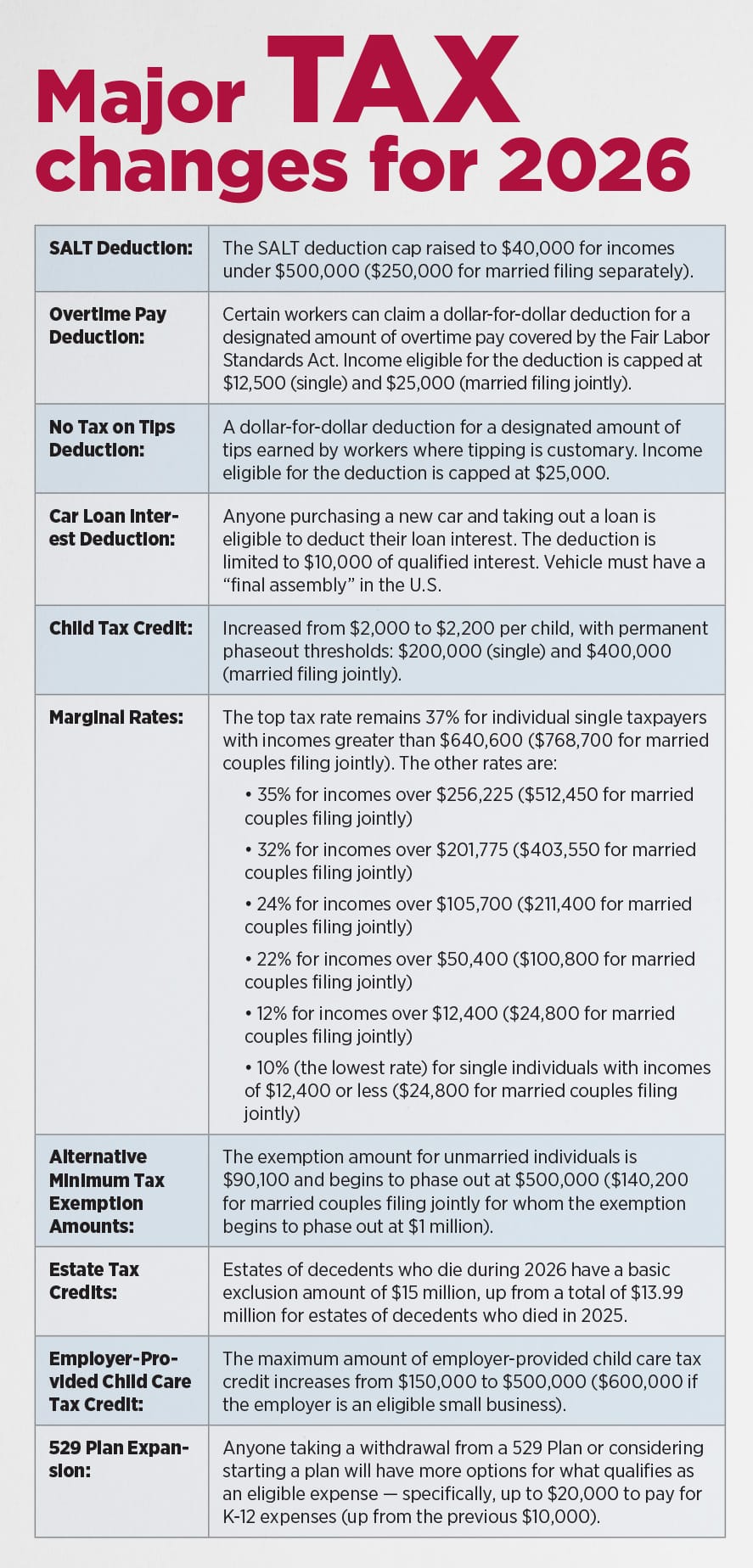

- Standard deduction is now $32,200 for joint filers, with the Child Tax Credit holding at $2,000 per child.

- The $10,000 SALT cap has expired—full state and local tax deductible in 2026 for high-tax-state businesses.

- Self-employed pros and pass-throughs retain the 20% Qualified Business Income (QBI) deduction.

- Credits reduce taxes dollar-for-dollar, deductions reduce taxable income—know the difference to optimize strategy.

- Strategic planning & documentation are vital for maximizing deductions and audit protection.

Welcome to 2026, where tax season just got a whole lot more predictable.

If you’ve been running a business or managing enterprise finances, you know uncertainty is expensive. The One Big Beautiful Bill Act changed the game in 2025, and now we’re seeing the results.

Think of OBBBA as the legislative equivalent of hitting “save” on your favorite tax benefits. Without it, we’d be facing a financial rollercoaster right now—rates jumping to 39.6%, standard deductions cut in half, and chaos for planning. Instead, business leaders can actually plan ahead. That’s not just convenient; it’s profitable.

Let’s break down what this means for your bottom line.

The Tax Landscape Business Leaders Need to Understand

Here’s what almost happened: the Tax Cuts and Jobs Act (TCJA) was set to expire at the end of 2025. Imagine prepping your entire financial strategy only to have the rules change overnight. Rates would have jumped from 37% to 39.6% at the top bracket. The standard deduction would have been sliced in half. Personal exemptions would have returned, complicating payroll calculations.

The OBBBA prevented that disaster. It made the favorable TCJA provisions permanent—lower rates, higher deductions, and business-friendly incentives stay put.

For additional context on how businesses prepared for the uncertainty surrounding the TCJA’s potential sunset, and key strategies to mitigate tax increases under the old scenario, see this strategic tax guide.

For the CEO managing enterprise finances, this means predictability. For the SME owner wearing multiple hats, it means one less headache. You can build five-year financial models without wondering if tax law will torpedo your projections in year two.

Consider this: one financial projection showed lifetime tax savings of $116,670 by avoiding the TCJA sunset scenario. That’s not pocket change—that’s a down payment on expansion, technology investment, or key talent acquisition.

Credits vs. Deductions: Know Your Weapons

Let’s clear up confusion that costs businesses thousands annually. Tax credits and tax deductions are not interchangeable terms. They’re completely different tools, and knowing which to prioritize can transform your tax strategy.

Tax credits are the heavy hitters. They reduce your tax bill dollar-for-dollar. If you owe $50,000 and claim a $2,000 credit, you now owe $48,000. Simple math, powerful impact.

Tax deductions reduce your taxable income. They’re valuable, but their power depends on your tax bracket. A $10,000 deduction in the 22% bracket saves $2,200. Same deduction in the 37% bracket saves $3,700.

Think of credits as direct discounts at checkout. Deductions are like reducing the price of items before calculating the final bill. Both save money, but credits pack more punch per dollar.

For 2026, understanding this distinction helps you prioritize. Chase credits first, especially refundable ones. Then optimize deductions based on your bracket and business structure.

Family Tax Credits That Impact Business Owners

Business leaders have families too, and family credits can significantly offset your tax liability. These aren’t small potatoes when you’re managing both business and personal finances.

The Child Tax Credit remains at $2,000 per qualifying child. Thanks to OBBBA, it didn’t revert to $1,000. For business owners with multiple children, this adds up fast. Two kids? That’s $4,000 off your tax bill directly.

The phaseout thresholds are generous: $200,000 for single filers, $400,000 for joint filers. Most SME owners fall within these ranges, making this credit accessible. Even successful enterprise executives often qualify.

Education credits continue unchanged. The American Opportunity Credit and Lifetime Learning Credit support higher education costs. If you’re funding college for children while running a business, these credits provide tangible relief during cash-intensive years.

The Earned Income Tax Credit (EITC) supports lower-income workers. While high-earning executives won’t qualify, businesses should understand it for employee education and retention strategies. It’s also relevant for side-hustle entrepreneurs building businesses while maintaining day jobs.

Here’s the business application: factor these credits into your compensation and distribution strategies. An S-corp owner deciding between salary and distributions should model how different income levels affect credit eligibility.

To see specific planning steps business leaders took amid the expiration risk of major credits, and to benchmark your approach, review this strategic analysis.

The Standard Deduction: Your Baseline Advantage

The 2026 standard deduction is $32,200 for married couples filing jointly. That’s a massive jump from pre-TCJA levels, and it’s now permanent.

Why should busy executives care? Because this is your baseline—the amount you can earn tax-free after other deductions. For business planning, it sets the floor for how you structure compensation.

Consider a married couple running an LLC. They can earn $32,200 before a single dollar gets taxed. Add in retirement contributions, health insurance deductions, and business expenses, and you’re building a powerful tax shield.

The strategic question: do you itemize or take the standard? For most businesses, the standard deduction is simpler and often more valuable. But high-tax-state businesses should run the numbers carefully, especially with recent SALT changes. For more guidance on this decision, including scenarios where itemizing beats the standard deduction due to state and local taxes or mortgage interest, see this planning guide.

The SALT Cap Expires: Big News for High-Tax States

If you operate in California, New York, New Jersey, or other high-tax states, listen up. The $10,000 state and local tax (SALT) cap expires in 2026. You can now deduct the full amount of state and local taxes.

This is game-changing for businesses in these regions. Previously, you hit the cap quickly with property taxes and state income taxes combined. Now? Full deductibility is back.

Let’s do the math. A business owner in California paying $30,000 in state income tax and $15,000 in property taxes couldn’t deduct $35,000 of that under the old cap. Now, all $45,000 is deductible. At the 37% federal bracket, that’s an additional $12,950 in federal tax savings.

The strategic play: if you’ve been deferring property tax payments or state estimated tax payments, 2026 might be the year to prepay. Bunch multiple years of deductible state taxes into one federal year to maximize itemized deductions.

For enterprise CFOs managing multi-state operations, this changes the calculus on where to locate headquarters and key operations. States with no income tax just became relatively less attractive from a pure tax arbitrage perspective.

To compare these strategies against the previous SALT cap environment and to ensure your business takes full advantage in 2026, see the full analysis.

Mortgage Interest: Still a Powerful Deduction

Homeownership remains tax-advantaged in 2026, which matters for business owners who often carry significant mortgages. Mortgage interest continues to be deductible, and with SALT cap expiration, the combined benefit is substantial.

Here’s why this matters for business leaders: many entrepreneurs leverage home equity to fund business operations. That mortgage interest you’re paying on the HELOC that funded your expansion? Still deductible, within limits.

The strategy: if you’re itemizing (likely, given SALT changes), ensure you’re capturing all mortgage interest. Properties used partially for business get additional deductions through home office rules, though these have changed.

Note that home office deductions for employees ended, but self-employed individuals and business owners can still claim them. If you run your SME from a dedicated home office, you can deduct that portion of mortgage interest, insurance, utilities, and maintenance.

For further insight into which home-related deductions survived post-TCJA, and to avoid missed opportunities or compliance errors, check the full rundown at this guide.

Self-Employment and Business Deductions: The QBI Goldmine

Self-employed professionals and pass-through business owners have a secret weapon: the Qualified Business Income (QBI) deduction. This lets you deduct up to 20% of qualified business income from certain pass-throughs.

Think about that. If your S-corp or LLC generates $200,000 in qualified income, you potentially deduct $40,000. That’s $40,000 of income that doesn’t get taxed at all. At a 24% marginal rate, that’s $9,600 in tax savings from one provision.

The QBI deduction was extended under OBBBA, giving businesses continued planning certainty. However, income thresholds and business type restrictions apply. Service businesses face additional limitations above certain income levels.

For a detailed breakdown of QBI deduction eligibility, phaseouts for service businesses, and comparison to 2025 transitional rules, refer to this in-depth breakdown.

Other critical self-employment deductions for 2026:

- Health insurance premiums: Fully deductible for self-employed individuals. If you’re paying $1,500 monthly for family coverage, that’s $18,000 in deductions annually.

- Retirement contributions: SEP-IRA contributions up to 25% of compensation. For high earners, this means $60,000+ in deductible contributions.

- Self-employment tax deduction: You can deduct half of your self-employment tax, reducing the sting of being both employer and employee.

The strategic application: structure your business to maximize QBI eligibility. This might mean separating service and product components, managing W-2 salary levels in S-corps, or timing income recognition.

Retirement Savings: The Long-Game Tax Strategy

Retirement accounts aren’t just about future security—they’re powerful current-year tax reduction tools. For business leaders, maximizing retirement contributions is non-negotiable tax planning.

401(k) contributions reduce taxable income today while building wealth. The ability to avoid the higher brackets that would have returned under TCJA sunset means permanent tax savings. Traditional 401(k) contributions come out pre-tax, lowering your current tax bill.

Roth options provide tax-free growth. For business owners expecting future income growth, Roth contributions mean you pay taxes now at lower OBBBA rates rather than potentially higher future rates.

Here’s a business owner scenario: You’re 45, running a successful SME, earning $300,000 annually. Maxing your solo 401(k) at $66,000 (2026 estimated limit) drops taxable income to $234,000. That saves roughly $15,840 in federal taxes at the 24% bracket, not counting state savings.

For enterprises, offering robust retirement benefits attracts and retains talent while reducing corporate tax liability. The Saver’s Credit also helps lower-income employees build retirement savings, improving overall employee financial wellness.

The strategic timing consideration: OBBBA’s permanence reduces the urgency to accelerate contributions before rate increases. However, younger business owners should still max out early-career contributions for maximum compound growth.

For background on how shifting legislation historically changed the “rush” to contribute and broader retirement planning strategy for owners and executives, visit this planning resource.

What You’ve Lost: Deductions That Disappeared

Not everything survived the tax law evolution. Understanding what’s gone helps avoid planning mistakes.

Home office deduction for employees is dead. If you’re a W-2 employee working remotely, you can’t deduct your home office. However, self-employed individuals and business owners retain this deduction.

Personal exemptions didn’t return. While TCJA eliminated these, the higher standard deduction more than compensates for most taxpayers. For large families, run the numbers—in some cases, the old exemption system was more favorable.

Some energy-efficient credits ended. If your business strategy included certain energy tax incentives, verify they’re still available. The landscape shifted, though many green energy incentives remain.

The lesson: tax planning requires staying current. What worked in 2024 might not work in 2026. Assumptions carry risk in tax strategy. For a list of what specifically was lost in the transition from TCJA sunset threats to OBBBA permanence, and how to pivot, see this resource.

Strategic Tax Planning for Business Leaders

Theory is useless without application. Here are concrete strategies for different business types:

For SME owners (under $5M revenue):

- Model your effective tax rate under different income scenarios. The difference between $200,000 and $250,000 in income might push you into different planning strategies.

- Bunch deductions into alternate years. If you’re close to the standard deduction threshold, consider prepaying deductible expenses to exceed it every other year.

- Time major purchases around your business cash flow and tax situation. Section 179 expensing and bonus depreciation create opportunities for year-end equipment purchases.

- Review your business entity structure annually. S-corp vs. LLC vs. C-corp tax treatment differs significantly, and what was optimal three years ago might not be today.

For enterprise executives:

- Maximize deferred compensation arrangements. These push income into lower-tax future years while providing current-year deductions.

- Review stock option exercise timing. OBBBA’s permanent lower rates might make exercising options earlier more attractive than under sunset uncertainty.

- Consider state residency planning. With SALT cap expiration, high-tax-state residency became more expensive in relative terms.

- Coordinate personal tax planning with corporate tax strategy. Your compensation mix (salary, bonus, equity, benefits) dramatically impacts total tax liability.

For all business leaders:

- Use tax projection software or hire professionals who do. Guessing costs money. Projecting saves it.

- Document everything. The IRS doesn’t accept “I’m pretty sure I spent that” as evidence. Receipts, mileage logs, and transaction records are non-negotiable.

- Plan quarterly, not annually. Tax surprises in April mean you missed opportunities throughout the prior year.

- Coordinate with your CPA before major financial decisions. Buying property, selling assets, or restructuring your business all carry significant tax implications.

To see real-world application of these tax planning moves under the 2026 legal landscape, and for up-to-date tactics, visit this comprehensive guide.

Documentation: Your Audit Insurance

You can execute perfect tax strategy, but without documentation, it’s worthless. Here’s what you need:

For credits: Form 1040 Schedule 8812 (Child Tax Credit), Schedule 8863 (education credits), and all supporting documentation. W-2s and 1099s must match your returns exactly.

For deductions: Keep receipts for itemized deductions, especially SALT payments and mortgage interest. Form 1098 documents mortgage interest; keep property tax bills. Self-employed individuals need Schedule C documentation—every business expense should have a receipt or invoice trail.

For QBI deduction: Document your pass-through income carefully. W-2 wages paid, unadjusted basis of assets, and business type classification all affect eligibility.

Retention period: Keep tax records for at least three years, though seven is safer for significant items. The IRS can audit up to six years back if they suspect substantial income underreporting.

The business application: implement systems now. Accounting software that categorizes expenses in real-time beats shoebox receipts every time. For enterprises, ensure your accounting team maintains documentation standards that exceed IRS requirements.

The 2026 Advantage: Stability Enables Strategy

Here’s what makes 2026 different from previous years: certainty. You can build multi-year tax strategies without wondering if foundational rules will change.

Compare 2026 to 2025. Last year, businesses faced potential TCJA sunset. Strategic planning required modeling two completely different tax scenarios. Resources went into contingency planning rather than execution. For a direct comparison of “double scenario” planning versus today’s one-track approach, see this analysis.

Now you can project with confidence. That five-year expansion plan? You can accurately model tax implications. Considering a business acquisition? Tax treatment is predictable. Planning executive compensation packages? The brackets are set.

For business leaders, predictability has dollar value. You can optimize rather than hedge. You can execute rather than wait.

Your Next Steps

Immediate actions:

- Schedule a meeting with your CPA or tax professional. Review your current tax projection for 2026 based on OBBBA provisions.

- Calculate whether itemizing beats the standard deduction with new SALT rules. High-tax-state businesses especially need to run these numbers.

- Review your retirement contribution strategy. Are you maxing out tax-advantaged accounts?

- Audit your business structure. Is your current entity type optimal under permanent TCJA provisions?

Quarterly actions:

- Review year-to-date income and expenses. Adjust estimated tax payments if needed.

- Evaluate opportunities for deduction bunching or income acceleration/deferral.

- Document major business decisions and their tax implications.

Annual actions:

- Complete a comprehensive tax planning review each fall, well before year-end.

- Consider year-end tax moves like equipment purchases, retirement contributions, or estimated tax prepayments.

- Update your multi-year financial models to reflect actual results and adjusted projections.

The 2026 tax season offers something rare in tax law: stability. The question is whether you’ll leverage it. The opportunities are clear—lower permanent rates, valuable deductions, and powerful credits.

Your competitors are already planning. The business leaders who master 2026’s tax landscape won’t just save money—they’ll redirect those savings into growth, talent, and competitive advantage.

Welcome to 2026. The rules are set, the opportunities are clear, and the strategies are proven. Now it’s time to execute.

Frequently Asked Questions (FAQ)

-

Are the TCJA lower tax rates now permanent?

Yes. The One Big Beautiful Bill Act made the TCJA rates (lower brackets, higher standard deduction, etc.) permanent so there will not be a “sunset” reverting to 2017 levels. -

Is the $10,000 SALT cap really gone?

Correct. Starting in 2026, you can once again deduct all state and local taxes paid if you itemize—huge news for residents of high-tax states. -

What is the QBI deduction and who qualifies?

The QBI deduction lets pass-through businesses deduct up to 20% of qualified income. There are income and activity limitations—see this QBI overview to check your eligibility. -

Can I still deduct my home office?

If self-employed or a business owner, yes. W-2 employees can’t. Deduct only true business-use expenses; document thoroughly. -

Do I have to choose between standard deduction and itemizing?

Yes, you must pick whichever provides more tax benefit each year. Use tax planning to evaluate which is best for you under the new laws. -

How long do I need to keep tax records?

Three years is the IRS minimum, but seven years is your safest bet, especially for significant deductions or if you underreported income by more than 25%.